HRA is granted by their respective employers. This allowance is basically a

part of employee’s salary package, in combination with all the terms and

conditions of their job. The Income tax act permits for deductions with respect

of the HRA given to the employee. The exemption on HRA Section 10(13A) covers

the exemption of HRA. The point here to be noticed is that HRA is partially

exempted.

An employee must pay rent for the house which he occupies,

to claim that expansion. It should be noted that the rented house or the

premises for accommodation must not be owned by him. If the person is staying

in his own house, then no amount is deductible. So, the overall amount of HRA

received is subject to tax. For all those who are getting paid monthly, the

most prevalent exemption comes out to be the allowance of their house rent.

House rent Allowance is basically to ensure the employees meet the necessary

expenses for their accommodation purposes. So that they meet the cost of their

rented house. But there are a lot of people who are claiming the rental

allowance using fake details. The circular have been revised to ensure that

only those people who are eligible for allowance should get them. Now, an

employee need to submit the PAN details of his landlord within the given time

limit.

The actual HRA received or the verifiable rent allowance received per month

by the employee will play the most crucial role for exemption. This will

reflect that how much allowance is actually being given by the employer.

SNo

|

Code

|

Conditions

|

1

|

A

|

Actual Rent Paid

|

2

|

B

|

A – 10% of Basic

|

3

|

C

|

50% Basic for Metro or 40% of Basic for Non Metro City

|

Click here to Download Automatic HRA Exemption Calculator U/s 10(13A)

You can avail HRA exception on the Minimum of the amount calculated between A,B and C.

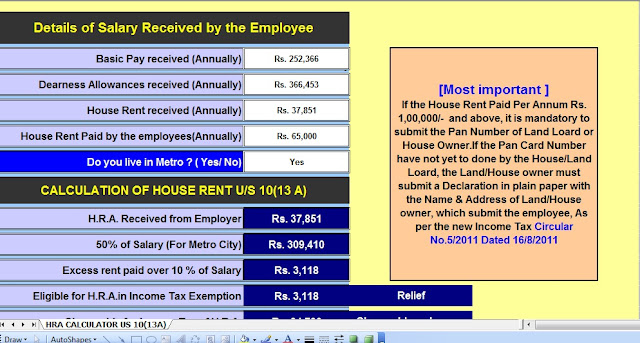

Land lord’s PAN detail’s Submission :

According to the previous circular issued, If all the assesses of employees

pay near Rs. 1,80,000 annually or 15,000 per month or above then that, then

employees are supposed to submit the PAN details of their landlord to their

employer. Then they will be able to avail the deduction in HRA.

But the revised circular no. 8/2013, issued by CBDT pronounce that, if the

rent paid is Rs.1,00,000 p.a or Rs. 8,333 per month or above than that. Then

submitting the PAN details is a compulsion for all. The Department has revised

the rule in order to avoid fake submission of rental payments to claim the HRA.

What if landlord does not have PAN?

What if your landlord does not have a PAN? Then for such employees, the

circular states that they need to submit a declaration. The declaration should

clearly state the same thing, but all the details of landlord must be mentioned

clearly. What landlord need to do is, during filing their return of income,

they have to indicate this rental income too. If he is not able to submit all

the details of the returned income and he fail to follow the rules. Then he

should be prepared to face the consequences. Because difficult circumstances

will definitely arise if the department comes around for the inspection. The

entire procedure should be done on time and the form should be completely

scrutinized and appropriate answers should be provided.

The circular states an exception too. There is no need to submit any receipt

as a proof of paid rent. This exception is only for that employee who receives

the rent allowance only up to Rs. 3,000 per month or 48,000 per year or below

that.

Rules are made to be followed, but sadly many of us fail to do so. The

result of any procedure depends on how we are executing it under the law. All

The required documents to avail the exemption should be sent to the Income Tax

Department. The deadline for submission is on or before February month ending

of approaching calendar year.

For any particular Violation in rules or delay they have to face the

consequences. The HRA deduction granted will eventually be reversed, this will

lead to addition of HRA amount to the overall income of the assets.

The entire procedure is simple, but it requires to follow particular rules

and regulations and submission of PAN details. If everything is done on time in

appropriate way, then surely your result will be fruitful.