During the Budget 2018, Finance

Minister inserted a new Section 80TTB. This allows a tax deduction of up to

Rs.50,000 with respect to interest income from FDs held by senior citizens. Let

see the features of this section.

FDs or fixed instruments are the major backbones of

many of the senior citizens. However, the majority of these fixed instruments

are not so tax efficient. Hence, to give some relief to senior citizens Finance

Ministry introduced this new Section 80TTB.

This amendment is effective from Financial Year

2018-19 or Assessment Year 2019-20.

Who is eligible to claim the deduction under Section 80TTB?

Senior Citizen who is holding the FDs with Banks,

Co-operative Banks and also in Post Offices and earning the interest income

from such deposits are eligible to avail the deduction under Section 80TTB.

Here, the meaning of senior citizen is an

individual resident in India

Firms, an association of persons or a body of

individuals are not allowed to claim the deduction under Section 80TTB.

Also, if a senior citizen claimed the deduction under

Section 80TTA (all individuals can claim up to Rs.10,000 deduction against the

interest income received from a savings account), then they are not allowed to

claim the deduction under Section 80TTB.

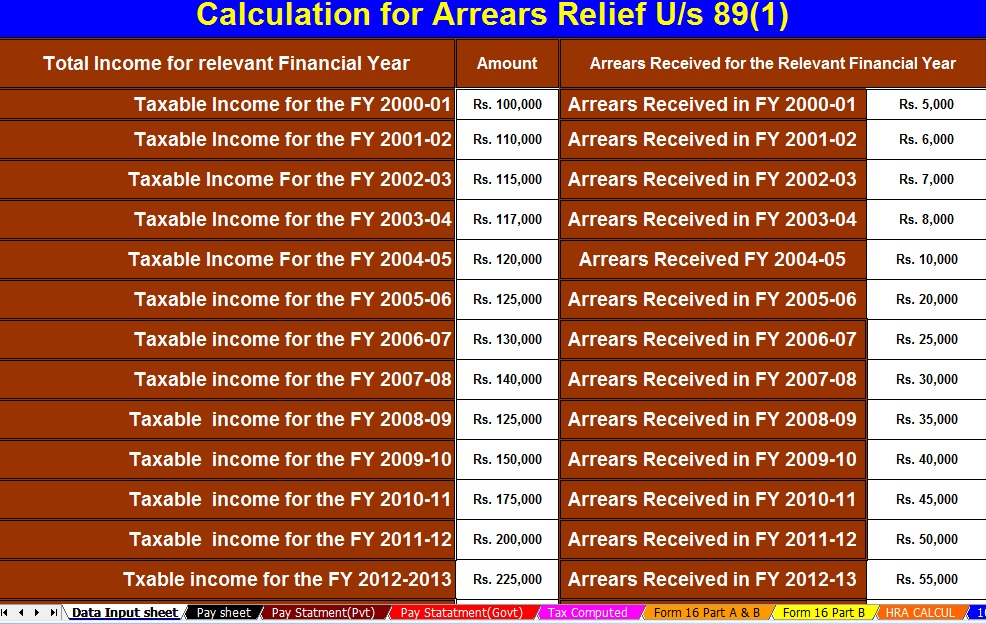

Click here to Download the Automated Income Tax Allin One TDS on Salary for Government & Non-Government Employees forF.Y.2018-19 & A.Y.2019-20 [ This Excel Utility can prepare at a time your Tax Computed Sheet + Individual Salary Sheet + Individual Salary Structure for Govt & Non-Govt employees salary pattern + Automated H.R.A. Exemption Calculation + Automated Arrears Relief Calculator with Form 10E from F.Y.2000-01 to F.Y.2018-19+ Automated Form 16 Part A&B and Form 16 Part B for F.Y.2018-19 ]

How much can we claim as the deduction under Section 80TTB?

As I mentioned above, if you are a senior citizen who

is holding the FDs with Banks, Co-operative Banks and also in Post Offices and

earning the interest income then you are eligible to claim up to the maximum of

Rs.50,000 in each financial year.

The maximum deduction allowed under Section 80TTB is

Rs.50,000. Hence, assume that you have Rs.45,000 as an interest income of FDs.

In such situation, you are allowed to claim only the actual interest income

(because the actual interest income is less than the maximum limit available

under Section 80TTB).

Same way, assume that you have Rs.60,000 as an

interest income from all FDs together. In that situation, as I mentioned the

maximum deduction allowable for deduction under Section 80TTB is Rs.50,000, you

can claim Rs.50,000 as the deduction. Rest of the Rs.10,000 will be your taxable

income.

Difference between Section 80TTA and Section 80TTB

There is a slight difference between Section 80TTA

and Section 80TTB. Hence, many get confused between these two income tax

sections.

Hope above information clears you

about Section 80TTB and also the difference between Section 80TTA and Section

80TTB.

{kind=link}